Despite the impressive growth of the global ṣukūk market, which has reached USD850 billion outstanding by 2023 and more than USD180 billion issuance in 2023, …

Despite the impressive growth of the global ṣukūk market, which has reached USD850 billion outstanding by 2023 and more than USD180 billion issuance in 2023, concerns remain about its compliance with Sharīʿah principles and ethical objectives. The main criticism is the dominance of debt-based sukuk structures such as murābaḥah and ijārah, which replicate the features of conventional bonds by relying on fixed income streams linked to underlying assets or leases.

Debt-based ṣukūk, particularly ijārah and murābaḥah, have historically accounted for the majority of issuance, marking at approximately 70-80% of the sukuk market value in 2022, according to the ICD-LSEG 2023 Islamic Finance Development Report. This is due to their simplicity and appeal to institutional investors. In contrast, equity-based ṣukūk (e.g. mushārakah and mudārabah) emphasize sharing of profits and losses and are more in line with Islamic risk-sharing principles, but account for a smaller share, estimated at 10-15% of total sukuk in 2022. This trend was also highlighted at the Al Baraka Symposium, held on 16-17 April 2025, in Madinah, Saudi Arabia. Prominent scholar Sheikh Abdullah bin Suleiman Al-Manea commented that nearly 90% of sukuk in the market may not be fully sharia-compliant due to their debt-like characteristics, and he called for a shift to asset-backed, equity-oriented structures to meet the industry’s ethical obligations.

The tendency of Islamic finance to mimic conventional finance further fuels criticism. Critics argue that Islamic financial products are often structured to closely resemble their conventional counterparts, raising questions about their compliance with Sharīʿah principles and their broader ethical purpose. For example, commodity murābaḥah-base tawarruq has been widely adopted for liquidity management, despite ongoing scholarly debates about its permissibility.

An additional aspect that is often neglected, yet warrants attention from stakeholders, is that although the ṣukūk market has expanded into the ESG sector, the fundamental structure of ṣukūk securitization has not changed. It primarily involves adjusting yield utilization to enhance its ‘green’ or ‘blue’ attributes, which may attract specific niche investors and market participants.

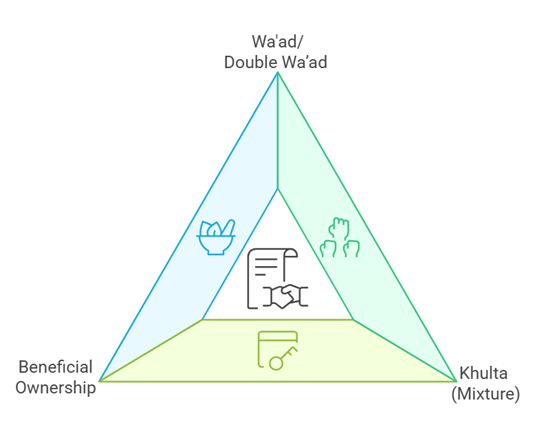

Izhar and Munkin (2021) identify three primary factors that contribute to the practice of Islamic financial engineering, making the Islamic capital market appear similar to its conventional equivalent. As Figure 1 shows, the first factor is the application of the wa’ad technique, particularly the double wa’ad, in Islamic financial contracts. The 2007 white paper by Deutsche Bank is considered one of the earliest documented discussions on the use of double wa’ad in modern Islamic financial engineering. The second factor involves the implementation of the concept of beneficial ownership (Haneef, 2005). And the third factor pertains to the application of the khulṭah (mixture) principle in commercial transactions.

Figure 1: Contributors to Islamic Financial Engineering in ICM

Source: Izhar and Munkin (2021)

The Islamic capital market, particularly through sukuk issuance, has significantly benefited from the adoption of these three concepts.

This mimicry has led to a compromised social impact, as the industry has yet to make significant strides in addressing issues like poverty alleviation or wealth inequality, which are central to the ethos of Islamic finance. It is argued that social objectives of Islamic finance, such as equitable wealth distribution and financial inclusion, have received less focus compared to commercial objectives. For instance, microfinance and waqf-based initiatives remains a relatively small segment of the Islamic finance landscape.

Ṣukūk market has undergone quite a significant evolution since its inception, adapting to the changing needs and dynamics of the global financial market and appetites of the stakeholders.

Figure 2: The Evolving Models of Ṣukūk

| Sequence | Model | Description | Key Features |

| 1st | Asset-backed Ṣukūk | The investors enjoy asset-backing, they benefit over some form of security or lien over the assets, and are therefore in a preferential position over other, unsecured creditors. |

|

| 2nd | Asset-based Ṣukūk | Ṣukūk holders will not have any security interest over the assets. The asset-based Ṣukūk are treated as senior unsecured securities similar to unsecured conventional bonds |

|

| 3rd | Blended-Asset Ṣukūk | Model #2The underlying assets consist of a mixture of tangible assets and debt/receivables |

|

| 4th | Asset-light Ṣukūk | Model #2 & #3The underlying assets are predominantly debt/receivables | Tangible assets ≤ 10% |

| 5th | ESG & Sustainability Ṣukūk | Ṣukūk structure where the proceeds are allocated to a mix of Sharīʿah-compliant green and social projects |

|

| 6th | Post AAOIFI Sharīʿah Standard 62 | Reverting to Asset-backed Ṣukūk? | Remains to be seen |

Source: Yağcı, Izhar, Abdul Manap (2025), Topical Issues #46, Islamic Development Bank

In February 2025, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) held public hearings on Sharīʿah Standard (SS) 62. This created a wave of discussion across the Islamic finance industry: Will there be a ‘tsunami’ in ṣukūk market in the wake of the issuance of AAOIFI Sharī‘ah Standard 62? For some, the new standard is perceived to be eventually shaking up the issuers by introducing complexities that would drive up costs and invite potential legal inconveniences, which potentially would alter the landscape of ṣukūk market altogether.

What has been the primary cause of concern is because SS62 prescribes a ‘true ownership’ on the part of the investors i.e. the ṣukūk certificate holders. Although the standard doesn’t clearly state the term, what is spelled out in clause 5-2-2, in essence, is about true ownership, as opposed to only the beneficial ownership by the certificate-holders. In other words, the certificate holders, under SS62, possess legal ownership since a ‘true sale’ is expected to occur in the process of ṣukūk securitization. This is contrary to the practice so far that entitled them to only use the asset ‘purchased’ without, however, becoming its legal owner.

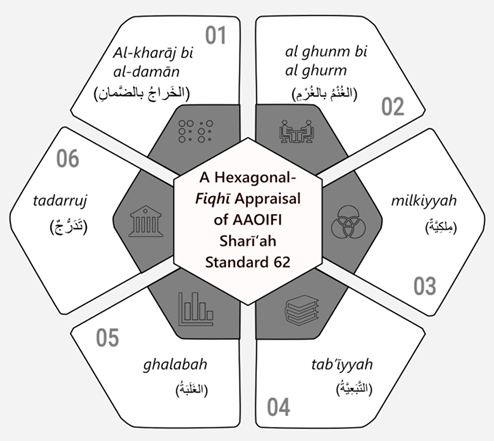

Figure 3: A Hexagonal-Fiqhī Appraisal of AAOIFI Sharī‘ah Standard 62

SS62 clearly sends a clear signal towards the implementation of assets-backed ṣukūk securitization. As such, the era of ‘beneficial ownership’ and assets-based ṣukūk may likely come to an end due this critical change in the ṣukūk standards.

Establishing a true legal ownership is congruent with the core Sharīʿah principles of al-kharāj bi al-damān and al-ghurm bi al-ghunm (labeled as #1 and #2 in Figure 3). The two principles are almost equivalent since ghunm is similar to kharāj and ghurm parallels to damān. Although SS62 only states al ghunm bi al ghurm briefly in the Clause 3-3, it is unfortunately silent on al-kharāj bi al-damān despite its enormous importance. The concept of tadarruj (principle#6 in Figure 3) can be adopted in a transition period until the market and its infrastructure set up are ready to adopt SS62.

The prospective implementation of AAOIFI SS62 presents potential significant changes for the ṣukūk market, possibly commencing from 2026. However, the ultimate impact remains uncertain, as it is contingent upon the standard’s final approval, specific content, and definitive implementation date.