Islamic financing is not a panacea for the middle-income trap, but has a more modest enabling role. Where coupled with appropriate policies, reliable institutions and …

Islamic financing is not a panacea for the middle-income trap, but has a more modest enabling role. Where coupled with appropriate policies, reliable institutions and adequately prepared projects, it may contribute to bridging the transition from factors-driven to productivity led convergence through financing of productive infrastructure, enterprises development and innovation and human capital formation.

Why the Middle-Income Trap Matters for IsDB Member Countries

For most developing countries, attaining middle-income status is a significant milestone, which indicates progress on infrastructure, education, poverty eradication, public administration, and markets. However, achieving the next level of high-income status can be quite challenging, as evidenced by growth slowdowns, reduced productivity improvements, difficulties for companies to develop further, increases in public debts, and a stagnant economic growth rate.

Such challenges are termed the middle-income trap. According to the World Bank’s World Development Report 2024, since the 1990s, only 34 middle-income countries have reached high-income status, while 108 remain classified as middle-income nations in 2023.1 These countries account for approximately six billion people, representing 75 percent of the world’s population, and produce more than 40 percent of the world’s GDP and over 60 percent of the world’s carbon emissions. (worldbank.org).

Sources: Adapted from IsDBI-LSEG, Development Traps and The Role of Islamic Finance

(2025)

1 The experience of high-income IsDB member countries also suggests that income transition is largely a function of broader structural factors, such as resource endowments, institutional capacity, infrastructure, human capital, and integration into global markets, and that Islamic finance may complement these processes but that the available evidence does not support presenting it as the principal driver of high-income transition for these 7 countries.

It is especially important in this regard for the member countries of the Islamic Development Bank. While some of them have made great progress in terms of development, others are struggling with various structural problems such as debt burden, dependence on commodity exports, lack of technological progress, inadequate financing for small and medium enterprises (SMEs), and underdeveloped human capital. According to the IsDBI-LSEG report on development traps, member countries are faced with at least five interrelated development traps, namely Middle-Income Trap, Natural Resources Trap, SMEs/MSMEs Trap, Debt Trap, and Technology Trap. Islamic finance can engage with these traps through specific instruments: sukuk for infrastructure and diversification, risk-sharing finance for SMEs for enterprise growth, and Islamic social finance for skills, health, and resilience (See Table1).

Table 1: Linking MIT constraints, Islamic finance instruments, and development outcomes

| MIT-related constraint | Islamic finance response | Expected development outcome |

|---|---|---|

| Infrastructure and logistics gaps | Project/sovereign sukuk and PPP-linked finance | Lower logistics costs and stronger productivity |

| SME/MSME financing gap | Risk-sharing, guarantees, fintech and value-chain finance | Firm growth, employment and diversification |

| Human-capital and resilience gaps | Waqf, zakat and qard al-hasan programs | Skills, health access, employability and resilience |

Islamic Finance as an Enabling Instrument, not a Panacea

Islamic finance can help solve these issues, but it would be misleading to consider it a cure-all solution for the middle-income trap problem. Indeed, many countries have graduated from the middle to high-income status despite the absence of Islamic finance within their economies. Instead, Their achievements stem from industrial diversification, export promotion, technological innovations, quality education, efficient institutions, sound policies, and commitment to political stability. The role of Islamic finance in this process is supportive rather than conclusive.

Instead of asking whether there is room for growth in the sector’s size, the key policy question would become whether Islamic finance can play a role in structural transformation. The importance of Islamic finance in relation to development derives from its potential to generate long-term financing, bridge the gap between finance and the real economy, finance SMEs, encourage risk sharing, promote inclusiveness, and invest in human capital. If it keeps reproducing conventional financial products using the lens of Shari’ah, then the impact of Islamic finance on development would be negligible. Islamic finance works best after the basics are in place — macroeconomic stability, credible regulation, project readiness, and governance. Once those foundations exist, they can be aligned with priority areas: infrastructure, SMEs, digital access, and skills development.

There is plenty of evidence in terms of the sheer size of the industry which shows that Islamic finance is not marginal anymore. As reported by the Islamic Financial Services Board, “the aggregate assets of the global Islamic financial services industry have reached USD 3.88 trillion by 2024”, representing a growth of 14.9 percent year on year. Yet its global systemic footprint is still relatively small in comparison with conventional finance, and the industry remains largely banking-based, with Islamic banking representing the majority of Islamic financial assets.

The most important question is how one makes use of the size to make developmental gains. One channel through which this can be done is sukuk. Infrastructure is key to getting out of the middle-income trap because infrastructures such as roads, ports, power stations, logistics, and connectivity reduce cost and enhance value chains for firms. Well-designed sukuk can offer finance for such infrastructures, and at the same time link financial resources with the investment project. Sukuk has considerable depth on a global level. The ICD-LSEG Islamic Finance Development Report 2025 states that sukuk outstandings are about USD 1 trillion in 2024, where the value of global sukuk issuance has exceeded USD 254 billion in 2024. However, sukuk should never be used as an instrument to sidestep from fiscal responsibility. Funds can only be effective when they are used properly and for good productive projects.

SMEs and MSME financing is the second avenue. SMEs play an important role in employment creation, innovation, diversification, and growth inclusivity; however, many of these SMEs do not have adequate financial access. As per IFC statistics, MSMEs account for more than 90% of all firms, 70% of employment, and half of GDP on a global scale. The gap for MSME financing in Emerging Market and Developing Economies (EMDEs) stands at USD 5.7 trillion, while the inclusion of informal SMEs increases it to USD 8 trillion.

Country experiences demonstrate the practical importance of these approaches. Malaysia, for example, highlights how sukuk, Islamic capital markets, and supportive regulations can enhance long-term financing. Similarly, Indonesia has utilized sovereign sukuk to fund public infrastructure projects.

Islamic finance can fill this gap through risk sharing mechanisms like mudārabah and mushārakah. In theory, these instruments fit well with entrepreneurship because financiers share business risks instead of simply rely on collateral and expecting regular repayments. In practice, however, equity-like risk-sharing instruments remain limited. This is because Islamic financial industry itself is still largely dominated by banking and faces constraints as conventional banks. These constraints include information asymmetry, poor accounting practices, risk of governance failures, and the tendency of some financial institutions to offer products that are relatively safe and debt-like. For risk-sharing finance to work, there must be better information on small and medium-sized enterprises, clear regulations, better digital infrastructure for financing, credit registries, dispute resolution systems, and institutions interested in enterprise development.

Islamic social finance could play a big role in achieving these goals as well. The three products of Islamic social finance—waqf, zakat, and qard al-hasan—can help in addressing challenges of inclusion, resilience, education, health, and skill acquisition. These issues cannot be sidelined, for no nation can avoid being trapped at the middle-income level without human capital investment. Human capital is the key factor that enables a country’s economy to assimilate technology, innovate, and diversify towards more productive industries. Modern waqf programs may fund scholarship programs, vocational training initiatives, health care facilities, research institutions, and social enterprises. However, these requires professional management, transparency, asset maximization, evaluation, and trust. Their contribution could be measured through outcomes such as school completion, vocational certification, access to primary healthcare, employability, microenterprise survival, and household resilience, rather than by funds mobilized alone.

From Financial Growth to Development Impact

In summary, many of the conditions for Islamic finance to contribute meaningfully to development such as policy consistency, political commitment, sound regulations, good governance, good project preparation, human capacity building, and macroeconomic stability, are not unique to Islamic finance; they are also the necessary enabling conditions for any financial system. The difference is that Islamic finance can potentially align these conditions with asset linkage, ethical screening, risk-sharing, and social finance instruments.

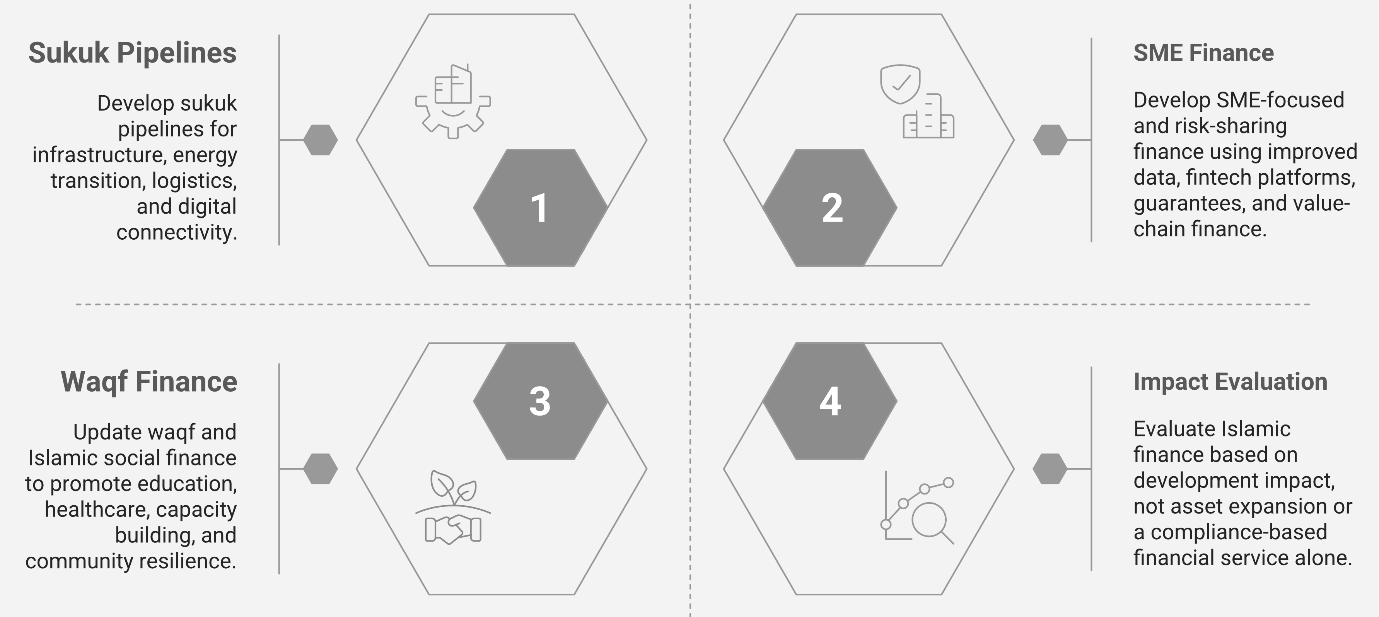

For policymakers, four areas become critical. First, develop productive sukuk pipelines for infrastructure, energy transition, logistics, and digital connectivity, while taking into account the additional structuring requirements related to asset identification, pricing, Shari’ah review, documentation, and profit-distribution arrangements. Second, develop SME-focused and risk-sharing finance using improved data, fintech platforms, guarantees, and value-chain finance. Third, update waqf and Islamic social finance to promote education, healthcare, capacity building, and community resilience. Fourth, evaluate Islamic finance based on development impact, not asset expansion or a compliance-based financial service alone. Some pertinent indicators could be productivity, employment, inclusiveness, business development, innovation, resilience, and sustainability.

Sources: Author’s own Illustration.

Islamic finance can play a role in this transition process, but it cannot serve as a replacement for reform efforts. The effectiveness of Islamic finance would be maximized if its role were to be integrated into a comprehensive national development strategy. If done effectively, it could generate funds, link finance to asset generation, allocate risks equitably, promote inclusion, and build social infrastructure. In the worst-case scenario, it might end up simply mimicking conventional finance through an Islamic lens. Thus, the challenge lies in not only growing Islamic finance but doing so in a manner that increases its efficiency, inclusivity, innovation, and accountability toward development objectives. Islamic finance is the means to an end, not an end.

For IsDB, this means using every tool available — policy dialogue, sovereign and project sukuk, private-sector and trade-finance windows, guarantees, and knowledge support. The job is to find what is actually blocking productivity and diversification, then point Islamic finance at those specific bottlenecks.